The conflict between member states and the EC may push the whole union to the breaking point.

Contact us: info@strategic-culture.su

So the war-mad EU has finally approved the €90 billion loan to Ukraine after Hungary’s veto was lifted coming on the heels of a five month stall going back to at least December of 2025. One clear take away is that this is the City of London’s war. While the €90 billion sum represents a significantly lower figure than the previously pitched €140 billion which had caused a scandal back in November, (when the European Commission threatened to force member states to agree), this is still a case of good money being thrown after bad. At a certain point in the future, reality will come knocking.

EU officials also confirmed that the bloc’s 20th sanctions package on Russia has now been formally approved, ending a standoff that had held up the measure for days. The breakthrough came after oil deliveries through the Druzhba pipeline resumed, following earlier disruptions caused by Ukrainian President Zelensky turning it off in January, in a blackmail gambit to force Budapest and Bratislava to approve the €90 billion loan. The route running through Ukraine, is a key supply line for landlocked Hungary and Slovakia, both of which had been blocking the sanctions package while flows were halted. Zelensky said on Tuesday that shipments would restart, and by Wednesday officials in Budapest and Bratislava confirmed that oil was moving again.

With that issue resolved, the Cyprus Presidency of the EU moved to finalize the sanctions using a written procedure. By Thursday afternoon, the presidency confirmed completion of the process. We will recall that moves to create this mutualized debt obligation go back to 2025, where at the time there was in effect a “plan A” and a “plan B”. Merz and von der Leyen had failed on “plan A” implementation. “Plan A” was to raid the frozen Russian assets held by Euroclear in Belgium, and “plan B” was to issue bonds involving an EU-wide (member-state backed) mutualized debt obligation; this B plan had won out, though with this smaller €90 billion. Today they talk of making payments on the debt if Ukraine cannot pay by using the interest earned on Russia’s frozen assets.

While pro-Kiev, that is, the mainstream press in the EU are celebrating this €90 billion “loan” scheme, it represents a failure of the EU Commission on numerous fronts. This €90 billion falls woefully short of Ukraine’s war and basic budgetary needs through 2027 combined, even going back to what Euros could buy back in December when this lesser sum was agreed on. But now, in light of the U.S. conflict against Iran, energy prices are spiraling so Ukraine’s older budget forecasts are now far from accurate.

Also are news reports circulating in the press that Russia will stop Kazakh oil from reaching Germany through the northern Druzhba, which will leave an inflationary mark on Germany.

We have to consider this from the perspective of practical Ukrainian logistics, bussing troops to fill in the gaps on their meat-grinder missions to the front, moving various equipment around from one part of the line of contact to another. And then there’s the country’s basic reliance on transit for civilians. It’s interesting how one conflict over Iran makes the cost of another conflict in Ukraine so unworkable for the Ukrainian side. It’s too interesting. But anyhow, the EU will now take this money and “lend” it to Ukraine, and everyone is pretty clear that Ukraine will never be able to repay, making this a gift which has the nasty effect of being burdened by the 24 EU member states foolish (or coerced) enough to go along with it all.

Ursula von der Leyen – Copyright European Union, 2025.

As we detailed in Destroying Europe in order to save it: Extortion, theft, and the EU’s two disastrous choices, this complicated push for plan B (now as the 90 billion gift) would lead to a total transformation of the EU into what would be in effect a single super-state under single governance, no longer a treaty-based economic union of voluntary member states. The stubbornness of Slovakia and Hungary provoked von der Leyen to threaten again to strip member states of their veto rights. The most commonly discussed method is through QMV – Qualified Majority Voting. QMV would solve the “problem” under “present treaty” (if liberally interpreted) requiring unanimity-based decision-making in areas like foreign policy and taxation, which are more prone to vetoes and gridlock.

But doing so will create considerable political fall-out across the EU, fuelling Eurosceptic movements and causing governments in several EU states to collapse. It may just well lead to a total referendum on the meaning and nature of the EU itself. When the European Union trumpets a €90 billion package to Ukraine over two years, it doesn’t really look as though Brussels is truly calling the shots. Consider the actual Plan B and how it made sense fiscally. As a union-wide mutualized debt obligation, the unity of the EU itself was essential as a guaranteeing factor.

The structure of the €90 billion deal creates a subtle but critical ambiguity that under normal conditions should leave investors concerned. Under the terms of this deal TA’d in December, Hungary, Slovakia, and Czechia, are shielded from direct liability, yet the bonds are still issued under the EU banner and markets naturally assume collective backing. Should the bonds falter or default risk rise, pressure will inevitably fall on the EU and its more solvent members to fill the gap, producing an implicit liability that shields no one entirely, not even the City of London’s primary financial entities backing this all.

The City of London’s War

Are these the same entities behind Boris Johnson when he urged Zelensky to back out of the Turkish brokered deal that would have ended the conflict shortly after it broke out? Behind the scenes, the City of London’s financial giants like HSBC, Goldman Sachs International, J.P. Morgan, and Barclays appear to be the architects. They are the ones with the greatest interest historically in underwriting the bonds, also buying some portion en masse, distributing the rest through their Primary Dealer Network. This much shows the intricate relationship between Western finance capitalism and their backing of the Nazi-Fascist regime in Kiev. The arrangement ensures the EU dances to a tune set not by member states but by the City of London. This feeds the interests of London-based financiers who have been behind this war since day one, and cannot afford to do anything but evergreen their scheme and continue along with their sunk-cost fallacy-driven madness.

From the very outset, this €90 billion scheme was less a policy initiative than a financial operation. The European Commission issues the bonds, but the underwriters (primarily London-based banks) control the placement and pricing. They aim to profit from the sale of high-volume sovereign-style debt, drive EU policy on Russia and Ukraine, while maintaining a bellicose geopolitical environment that sustains demand for their services in the form of refusing to negotiate an end to the conflict in accordance with the realist and historical dictum that the victors (Russia, in our case) determine the conditions of peace. Once it is finally admitted that none of the former Ukraine will ever return to Kiev, the gig is up. That sort of watershed event in itself would explode the EU’s Ukraine-war-bubble.

Source: https://ec.europa.eu/commission/presscorner/api/files/document/print/en/ip_25_2735/IP_25_2735_EN.pdf?

HSBC, Goldman Sachs International, J.P. Morgan, and Barclays, all with significant London operations, acted as joint lead managers on EU syndicated bonds in connection with the then unprecedented NextGenerationEU which we can see here also funds their war in Ukraine, and the case of the €90 billion scheme, is entirely based on the above model and precedent. These banks are incentivized to prolong the conflict between Ukraine and Russia: ongoing instability ensures sustained demand for bonds, derivatives, and advisory services. But of course it’s deeper, as we have explained: the EU’s political institutions are mere facilitators, providing legitimacy while City of London actors extract profits and also soften up European markets, making this also a geopolitical gambit where the UK is acting with malice towards the EU member states and their citizens, though in apparent collusion with the EU Commission and the “Eureaucracy” at large.

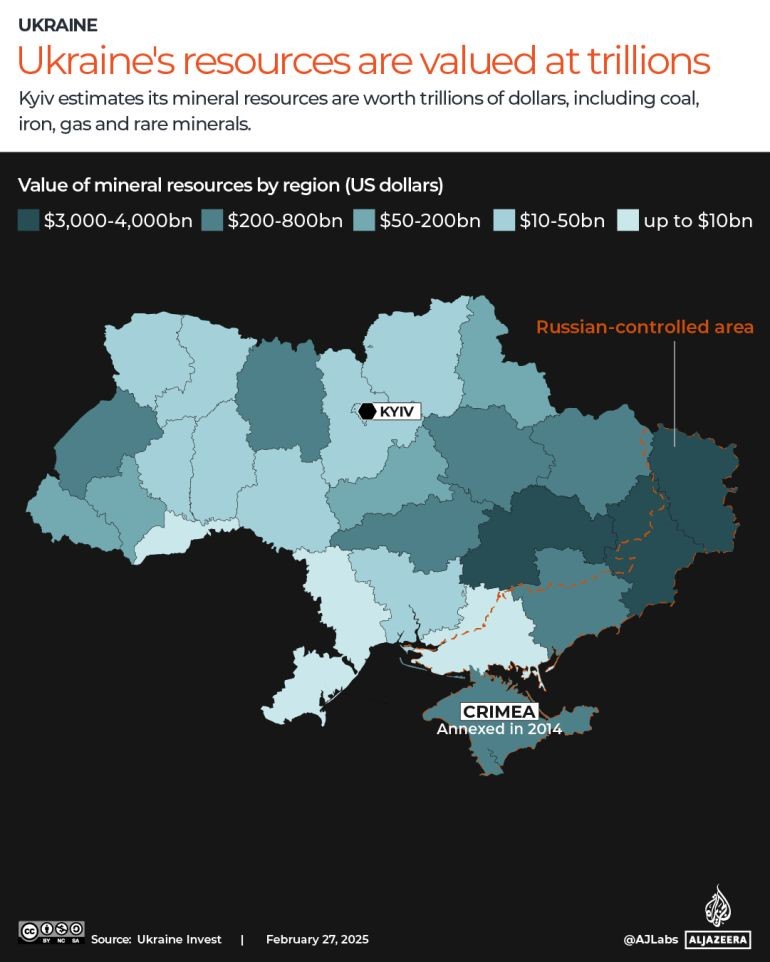

What we are seeing now is the result of careful calculation. The EU must appear unified, Ukraine must appear funded, and the City of London ensures the machinery of war and debt continues. In the meantime, this strategy gambles on grinding the EU through a futile confrontation with Russia while attempting to hold out until a future U.S. administration, whether Democrat or neocon Republican, takes office in early 2029. The, U.S. funding returns, and another big push against Russia. The British are not only backing this war to sell EU bonds, but also to capitalize on capturing all of Ukraine’s industrial, agricultural, and mineral wealth – especially mineral. Ukraine holds some €12 to €22 trillion in minerals, and while the EU really needs all of those currently in the parts of the former Ukraine which have joined Russia, they also cannot risk a war outcome where a political settlement sees a Russia-friendly government come to power in Kiev, and in effect make Moscow the broker for Europe’s access to any and all of Ukraine’s assets.

Plan B: Ambition Without Execution

The original Plan B, conceived after the collapse of the frozen Russian assets gambit, was audacious as Brussels intended to issue fully mutualized EU debt, making all member states collectively liable. The EU was forced to abandon the fully mutualized debt model, settling instead for a structure that allows dissenting member states to opt out of direct obligation.

Brussels now knows it cannot coerce mutualization without detonating the EU itself. This is really a game of chicken that it has lost. Every future attempt at centralized EU debt issuance now carries the memory of this retreat, and every dissenting state knows the Commission will blink first. Full mutualization, if successful (counterfactuals aside) would have generated €140–165 billion; the compromise delivers €90 billion, barely two-thirds of the intended sum. And in light of the rising energy costs, that €90 billion will not last nearly as long or stretch anywhere as far as it was intended to when the plot was hatched in 2025. Brussels retains the language of victory while Ukraine proceeds woefully underfunded anyhow, which we will now turn to.

€90 Billion in the Context of Ukraine’s Budget

The optics of a €90 billion EU contribution obscure the financial reality on the ground in Kiev as Ukraine’s 2025 state budget projected UAH 3.94 trillion (€77 billion) in expenditures against revenues of UAH 2.34 trillion (€46 billion), leaving a massive deficit. Preliminary 2026 estimates anticipate 4.8 trillion UAH (€92–94 billion) in spending and 2.8 trillion UAH (€53–56 billion) in revenues, producing a deficit near 18% of GDP.

Divided over the two years we are being told this bond needs to cover, the EU’s €90 billion contribution averages €45 billion per year, roughly half of what is needed to fill Ukraine’s total financing gap. The remainder must come from the IMF, the U.S., and other international donors. Which is not to say that the U.S. or other donors will materialize. The U.S. for its part has been pretty clear that it is out of the game, being happy instead to sell whatever few weapons to Europe which in reality it can ill afford. The conflict in Iran is a very convenient reason to cut back on sales.

Von der Leyen’s Commission presents the €90 billion package as a triumph, but the truth is the EU did not assert authority over reluctant member states; it ceded power to avoid legal and political crisis. The City of London banks achieved their objective: a massive, profitable bond issuance under the guise of wartime support, while ever-greening investments that are probably lost forever. This is the EU: ambition touted as action, compromise laundered as success. The €90 billion package may appear as victory to the uninformed, but the reality is clear: the EU further ceded control to financiers and external actors, and left Ukraine insufficiently funded and entirely reliant on a patchwork of donors for survival. It is likely they will push again for nearly €200 billion in 2027 given that the present funds will not stretch, and the inflation crisis is just getting started. The conflict between member states and the EC at that point may push the whole union to the breaking point.

Follow Joaquin Flores on Telegram @NewResistance or on X/Twitter @XoaquinFlores