Friedrich Merz won’t survive a single term in office and France will be the next country to exit the EU, triggering an implosion of the project.

Join us on Telegram![]() , Twitter

, Twitter![]() , and VK

, and VK![]() .

.

Contact us: info@strategic-culture.su

Europe will either continue the war at huge cost to avoid a reckoning with its disastrous policy towards Russia, or end the war, and face the prospect of Ukrainian membership which will tear the EU apart. No wonder the Eurocrats are bang out of ideas and throwing out more pointless sanctions.

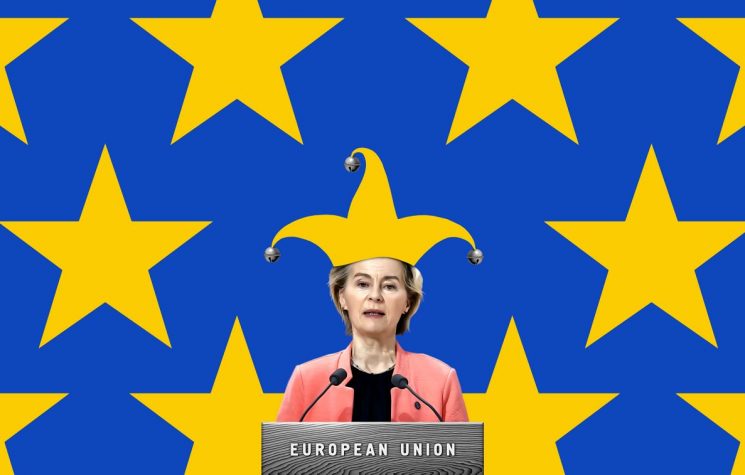

Few things characterise the emptiness of European energy policy that Ursula von Der Leyen’s announcement that the Nordstream 1 and 2 pipelines would be hitherto banned. In what has been described as a significant escalation, she announced on X that ‘Europe is putting Nordstream 1 & 2 behind for good.’ Both pipelines lay empty, and some were destroyed by a terrorist attack in September 2022. Nothing says escalation less than a sanction with zero economic cost.

And this latest move also signals increasing desperation in Europe about what to do about Russia, in circumstances where no one wants to fight Russia. The arrival of Friedrich Merz as German Chancellor has undoubtedly shifted the centre of gravity of EU policy towards Berlin, as he tries to position himself as the tough kid on the block.

But I want to be the first to predict that Merz won’t survive a full term in office.

The weight of domestic concern in Germany about self-defeating foreign policy is turbo-charging the growth of AfD which has become Germany’s most popular party since the February elections, according to polls.

As I, and many others, have said before, European industry has been crippled by high energy prices, and we are told, this is Russia’s fault. But it is manifestly driven by self-defeating energy policies in Brussels and Berlin. Rather cutting energy connections, the only answer is to boost global supply which would inevitably bring uncomfortable choices about Russian pipelines back to the table. Should this happen, von der Leyen’s credibility and Merz’s honeymoon in office, would suffer a cold shower.

Taking every step possible to delay or prevent a ceasefire in Ukraine simply kicks the sloshing bucket of iced water further down the slippery bathroom floor.

Yet citizens suffering under the weight of high prices will still remember that before the war started, gas prices in Europe were extremely low – comparable to U.S. gas prices today – because of hugely favourable global supply. LNG from the U.S., the Middle East and Africa together with piped gas from Norway and Russia, pushed the wholesale price of gas down to levels not seen since 2005.

European LNG imports had risen sharply after the onset of the Ukraine crisis in 2014 increasing from only 10% of to nearly 50% today, while Russian piped gas kept flowing. As part of this, imports from the U.S. tripled in volume between 2021 and 2023 and they now make up almost 50% of total European LNG imports.

Cutting Russian gas pipelines has had a devastating effect on the European supply equation.

Read the European press and you’ll hear often how U.S. LNG is too expensive, which contributes to the economic headwinds manufacturers in Germany and else are facing. Emmanuel Macron has in the past called out the U.S. as ‘unfriendly’ for selling expensive LNG. But this is deeply misleading.

Back in 2019, there was more gas than the world could possibly use, bearing down on prices. The fact of piped or shipped was immaterial to the glut in supply. The surge in U.S. supplies was doing to global gas prices what the glut of U.S. shale oil was doing in January 2016 when prices sunk to $26 per barrel.

The 2016 oil price collapse put immense pressure on Russia’s economy, which is heavily reliant on tax from oil and gas exports. Russia’s current account surplus in 2016 hit its lowest level since 1999, pinching tax income significantly. And that was at a time when Russia was pumping record amounts of oil and gas.

Because herein lies a truth; the global price of energy has a much bigger impact on Russia than the amount of energy that you buy from Russia.

When President Trump talks to OPEC about slashing the oil price, and, by extension, the gas price, he thinks that this will damage Russia’s economy more than cutting Russian supplies

However, Russian monetary policy today is very different to 2016. A low rouble is embraced which helps to offset energy price slumps and brings in bigger surpluses when prices soar.

That’s why the second strand of von der Leyen’s grand plan – getting the G7 to agree to reduce the oil price cap from $60 to $45 – may also not work. And, in any case, G7 agreement to this will only be possible if the United States agrees. While Trump has spoken often about reducing the oil price by boosting global supply, it is far from clear that he will sign up to imposing another exogenous sanction on Russia, at a time when his administration is looking to reset relations with the Kremlin.

Mothballing Russian pipelines as putative punishment for Putin’s war in Ukraine is having the opposite effect – restricting supply, pushing up prices and hurting Europe far more than it is hurting Russia.

And, of course, Europe finds itself caught in a perfect storm of bad economic options. Continue the war at a huge economic cost, to delay the inevitable reckoning with its self-defeating policy with Russia. End the war and face an even bigger political and economic cost of admitting Ukraine as a member.

I have said before, admitting Ukraine to the EU would shake the financial foundations of the bloc and cause such widespread resistance, that Ukraine could only join on second-class terms and conditions. Specifically, countries like France and Poland will block and delay to avoid handing their generous subsidies to Kyiv.

It should come as no surprise that the newly elected President of Poland, Karol Nawrocki, has already said that Ukraine should not be admitted to the EU. He is not alone. Hungary’s Prime Minster Viktor Orban has long said that Ukraine’s accession to Europe would be an economic disaster.

It might be for some EU countries. The bigger problem, if you consider it a problem, is that it would cause a political disaster and an unravelling of the European project. What is happening political in Germany will, too, happen in France, and the lawfare against Le Pen will only accelerate that. It’s now a matter of when, not if, National Rally runs the government in Paris. When that happens, expect to see an increasingly nationalist France head for the exit triggering an implosion of the project.

Only radical reform, slashing the EU institutions and handing sovereignty back to member states can prevent this from happening. The chances of that, right now, appear very low.